“The first thing we do, let’s kill all the lawyers accountants.”

These words were not spoken by the butcher in Shakespeare’s Henry The Sixth Part 2, rather they are from the mouth of a new treasurer of a not-for-profit association or registered charity who mistakenly thought that taxes and not-for-profit are mutually exclusive.

Unfortunately, “exempt from tax under Part I of the Act” refers only to taxable income.

Sales Tax Rates in Provinces and Territories That Apply to Associations and Registered Charities

Effective October 1, 2016 the sales tax rates are as follows:

| Province | GST/HST | PST |

| British Columbia | 5% GST | 7% |

| Alberta | 5% GST | 0% |

| Saskatchewan | 5% GST | 5% |

| Manitoba | 5% GST | 8% |

| Ontario | 13% HST | n/a |

| Québec | 5% GST | 9.975% |

| Newfoundland and Labrador | 15% HST | n/a |

| Nova Scotia | 15% HST | n/a |

| New Brunswick | 15% HST | n/a |

| Prince Edward Island | 15% HST | n/a |

| Northwest Territories | 5% GST | 0% |

| Nunavut | 5% GST | 0% |

| Yukon | 5% GST | 0% |

Prince Edward Island will increase its sales tax from 14% to 15% effective October 1, 2016.

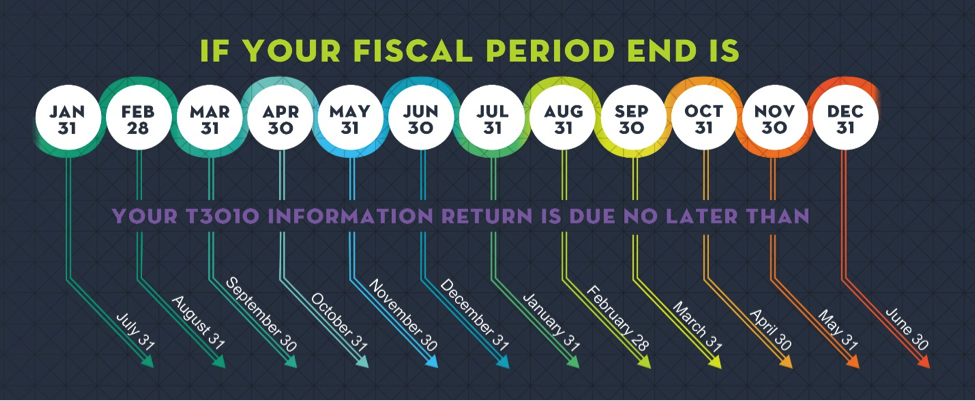

Canada Revenue Agency Filing Dates for a Registered Charity

Registered charities must file a Registered Charity Information Return, form T3010, annually with the Canada Revenue Agency (CRA), within six-months of your organization’s fiscal year end.

CRA, on August 4, 2016 wrote that its “Charities Directorate is introducing new ways to encourage voluntary compliance in the charitable sector. Registered charities have core responsibilities, one of which is to file an annual information return within six months of the charity’s fiscal year-end. If they do not file, they may lose their charitable registration [emphasis added]. We have recently developed a new infographic to help charities remember their filing deadlines, (as some treasurers cannot count to six).

New Reporting Requirement

“As a result of the 2015 Federal Budget, all registered charities must now annually report [limited] partnership holdings. Charities with a fiscal year end of December 31, 2015, will receive an insert 15-122: New reporting requirements as part of their annual return package. Charities with fiscal years ending in 2016 will see a new question on partnership holdings included in Form T3010 (16).”

GST/HST Rebate for Registered Charities

Registered charities apply for a rebate for a portion of the GST/HST that they paid, using Form 66 66. “If you are claiming a rebate of the provincial part of the HST (line B) use Form RC7066 SCH, Provincial Schedule – GST/HST Public Service Bodies’ Rebate.”

If your registered charity paid GST/HST in more than one province and/or territory, then you must record the sales tax paid, by province and/or territory.

To help ensure that registered charities correctly file Form 3010 within six-months of your yearend, CRA has changed its rules. You can now file an application for more than six-months, effective January 1, 2016.

Registered Charities Incorporated in Ontario?

“If you are incorporated in Ontario and subject to the Ontario Corporations Act, you must also include one of the following:

• Form RC232-WS, Director/Officer Worksheet and Ontario Corporations Information Act Annual Return

• Form RC232, Ontario Corporations Information Act Annual Return

“Form RC232, Ontario Corporations Information Act Annual Return, can only be submitted with the charity’s annual T3010, Registered Charity Information Return. The RC232 will not be accepted if it is submitted to the CRA without the applicable Form T3010 or if it is submitted directly to the province of Ontario [Ministry of Government Services].”

Québec Sales Tax

If your organization is planning to host an event in Québec, then it must register to collect Québec Sales Tax (QST), even if it is not registered to collect GST/HST.

For more information about QST please see our article GST/HST and QST – Do You Know What to do for Québec Events and Members?

Annual Corporations Canada Requirements

If your organization is incorporated federally, then you can learn your Corporations Canada filing obligations in our article Key Timing Milestones under the Canada Not-for-profit Corporations Act.

Provincial/Territorial Registrar Requirements

If your organization is incorporated by a province or territory, then you must provide information each year to your Provincial/Territorial Registrar. Contact information can be found at Corporations Canada’s website.

If your organization is not incorporated, then it is likely that you must also provide information to your Provincial/Territorial Registrar.

Contacting CRA about Changes in Your Board Membership

Whenever there is a change in directors, then you must advise CRA.

There is no form to advise CRA about the change in directors; however, they will accept Corporations Canada’s Form 4006 – Changes Regarding Directors, if your organization is incorporated federally. If you are not incorporated federally, then send to them the form that you have provided to your provincial/territorial registrar.

It is recommended that you submit a new Business Consent Form RC59 at the same time as you file your annual return. The individuals whose names appear on this form are the only ones that CRA will speak with about your organization.

In addition to listing board members who can contact CRA on your behalf, it is recommended that the law firm and your auditor’s/external accountant’s name be included.

If your organization is a registered charity, then it is recommended that you send a copy of the information you sent to CRA to the Charities Directorate. The Charities Directorate is part of CRA; however, the Charities Directorate does not receive all of the information sent solely to CRA.

As an association management company and as event managers, we present the above article for informational purposes only. It constitutes general information and does not constitute legal, income tax, or other professional advice.